We are using the DataAccess.TimeSeries - in fact our code comes from the TimeSeriesDailyIntervalDemo. Our client has discovered that there are several unwanted trade types that are returned by the API that are not displayed in the standard EIKON price charts. Upon request from Eikon we were advised that:

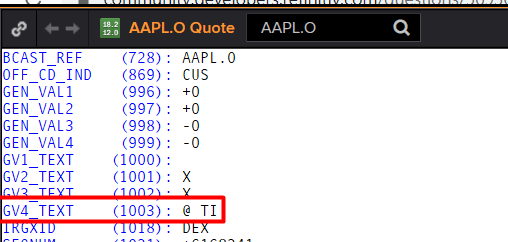

"Below are the criteria for the FID 1003 to exclude or to filtered out trades from TAS application.

Unique ID IDN Value Description

152526 1_N Next Day Trade

152540 4_B Average Price Trade

152542 4_M Market Center Official Close

152543 4_Q Market Center Official Open

152544 4_H Price Variation Trade

154580 2_9 Official Consolidated Close

152549 4_I Odd Lot trades

152525 1_C Cash Trade (Same Day Clearing)

152527 1_R Seller

152536 3_T Extended Hours Trade

152537 3_U Extended Hours Sold (Out of Sequence)

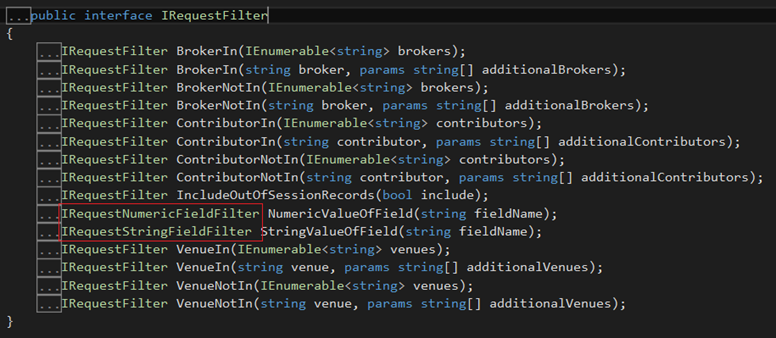

Can anyone advise how this should be coded in the API. We see a "WithFilter", but do not know the syntax to construct a filter to remove the above.

Thank you