For a deeper look into our DataScope Select REST API, look into:

Overview | Quickstart | Documentation | Downloads | Tutorials

1

●1 ●1 ●0

How to extract all LIBOR rates(USD, GBP, CHF, EUR, JPY) with all 7 different maturities(Overnight, 1 week, 1 month, 2 month, 3 month, 6 month, 12 month) by sending request to DSS REST API? Please give an example, urgent.

Hello @beatgtech

Thank you for your participation in the forum. Is the reply below satisfactory in resolving your query?

If so please can you click the 'Accept' text next to the appropriate reply. This will guide all community members who have a similar question.

Thanks,

AHS

Hi,

Please be informed that a reply has been verified as correct in answering the question, and has been marked as such.

Thanks,

AHS

11.3k

●25 ●9 ●14

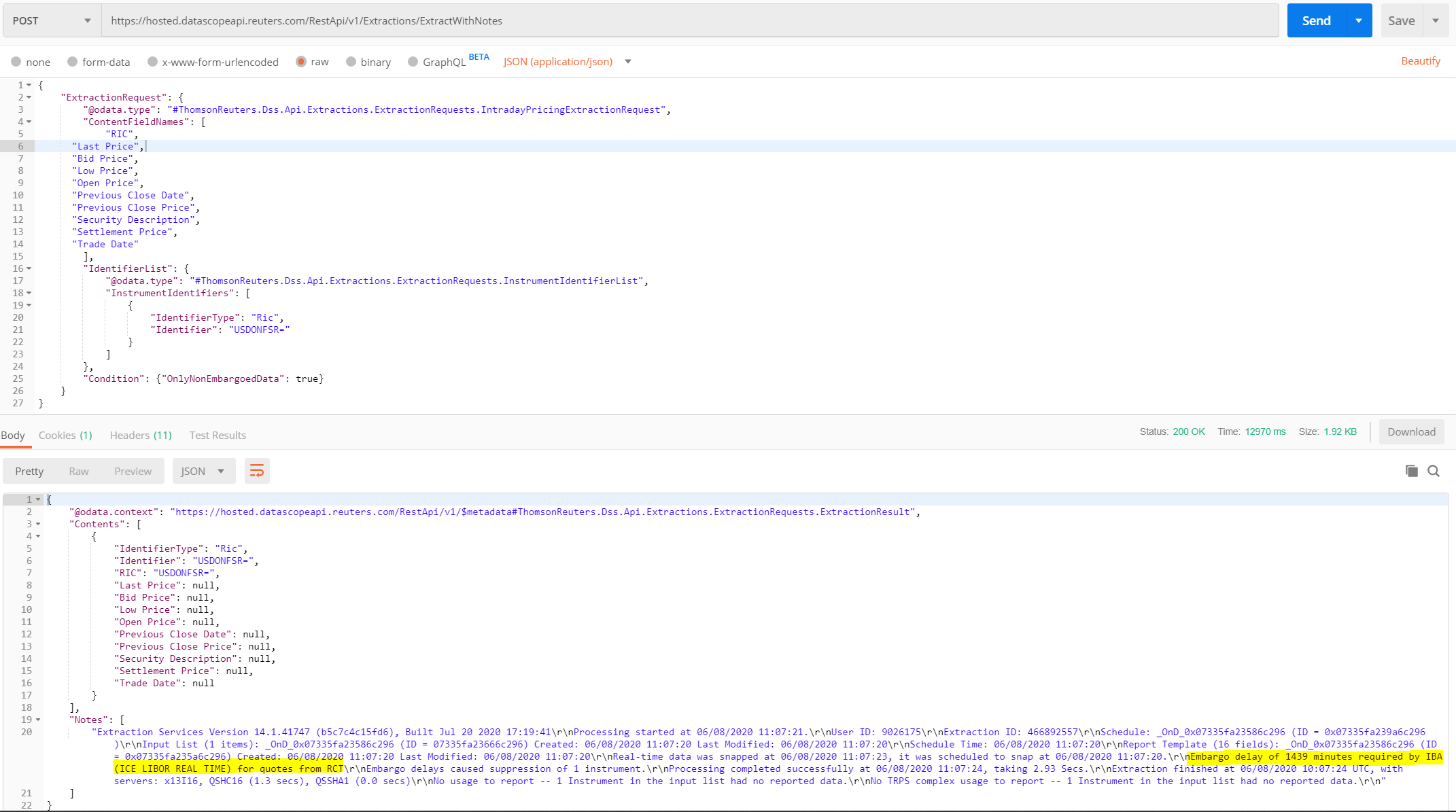

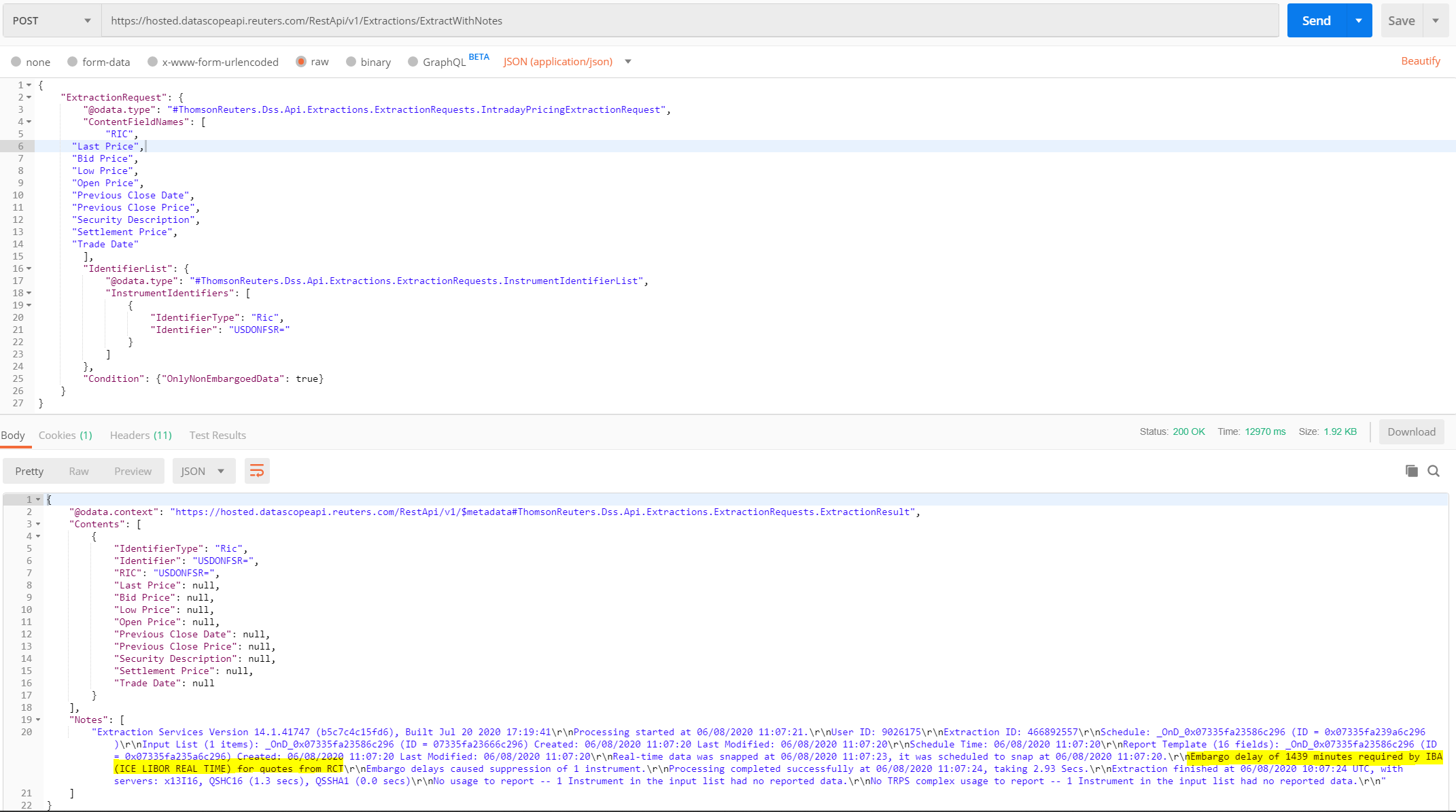

The rates and maturities could be identified using RIC name. For example, USD overnight rate, the RIC should be on USDONFSR=. If the extraction takes tool long to complete, it possibly is due to embargo. Please find more information in this tutorial.

Anyway, you can try the /LIBOR=which is delayed RIC. The delayed RIC is not affected by embargo.

Below is the request sample.

{

"ExtractionRequest": {

"@odata.type": "#ThomsonReuters.Dss.Api.Extractions.ExtractionRequests.IntradayPricingExtractionRequest",

"ContentFieldNames": [

"RIC",

"Last Price",

"Trade Date"

],

"IdentifierList": {

"@odata.type": "#ThomsonReuters.Dss.Api.Extractions.ExtractionRequests.InstrumentIdentifierList",

"InstrumentIdentifiers": [

{

"IdentifierType": "ChainRIC",

"Identifier": "/LIBOR="

}

]

}

}

}

all fields are null...

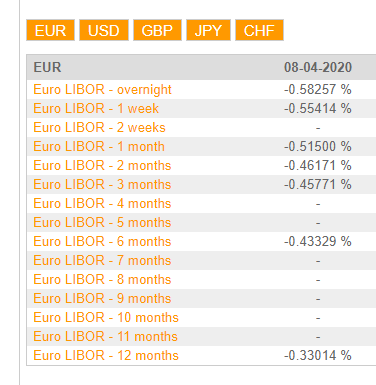

These are LIBOR rates I queried from other websites. So what the request template should be if I want to retrieve today or yesterday LIBOR rates (in 7 maturities (from overnight to 12 months) and in 5 different currencies mentioned in the question) ?

@beatgtech,

As you can see, the Notes fields indicates that the extraction was embargoed because your account doesn't have permission for ICE LIBOR Real-time. You will get the extracted data after 1439 minutes. Please contact your Refinitiv account manager for the permission issue.

Anyway, you can try the /LIBOR= RIC instead for previous day data.

11.3k

●25 ●9 ●14

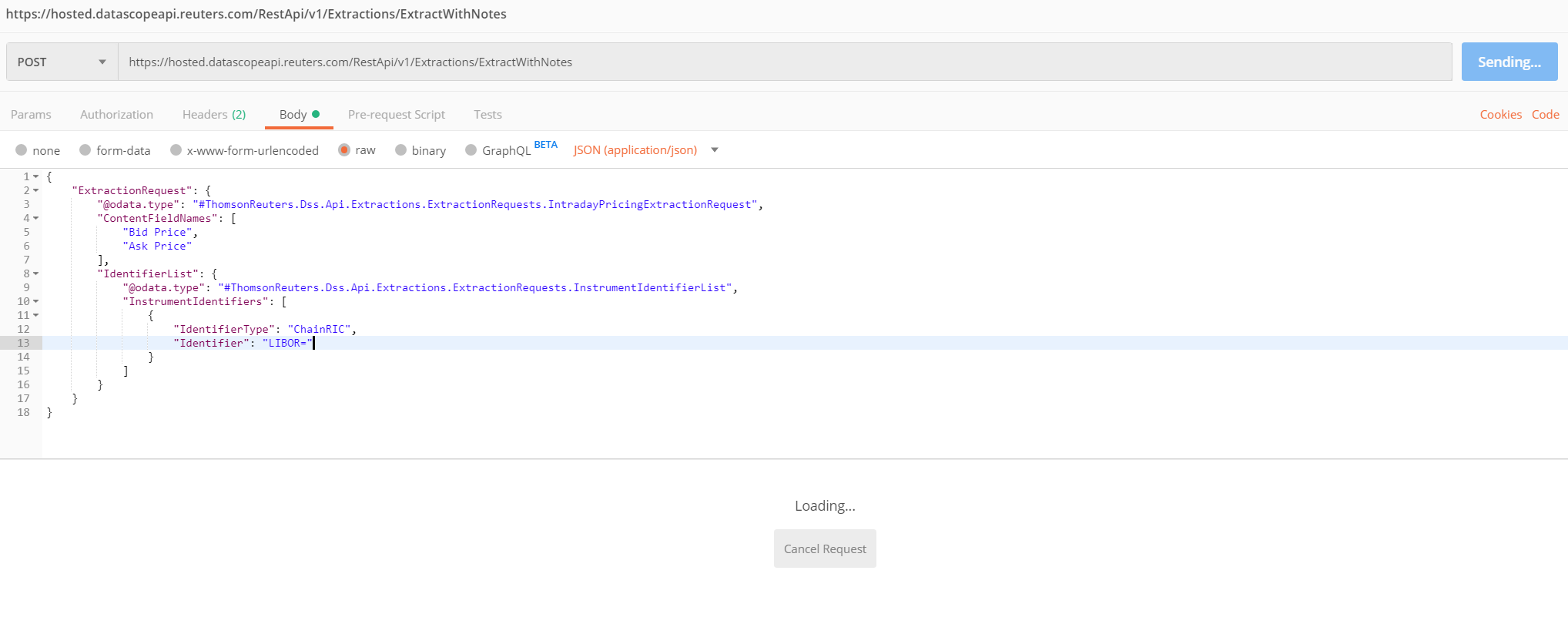

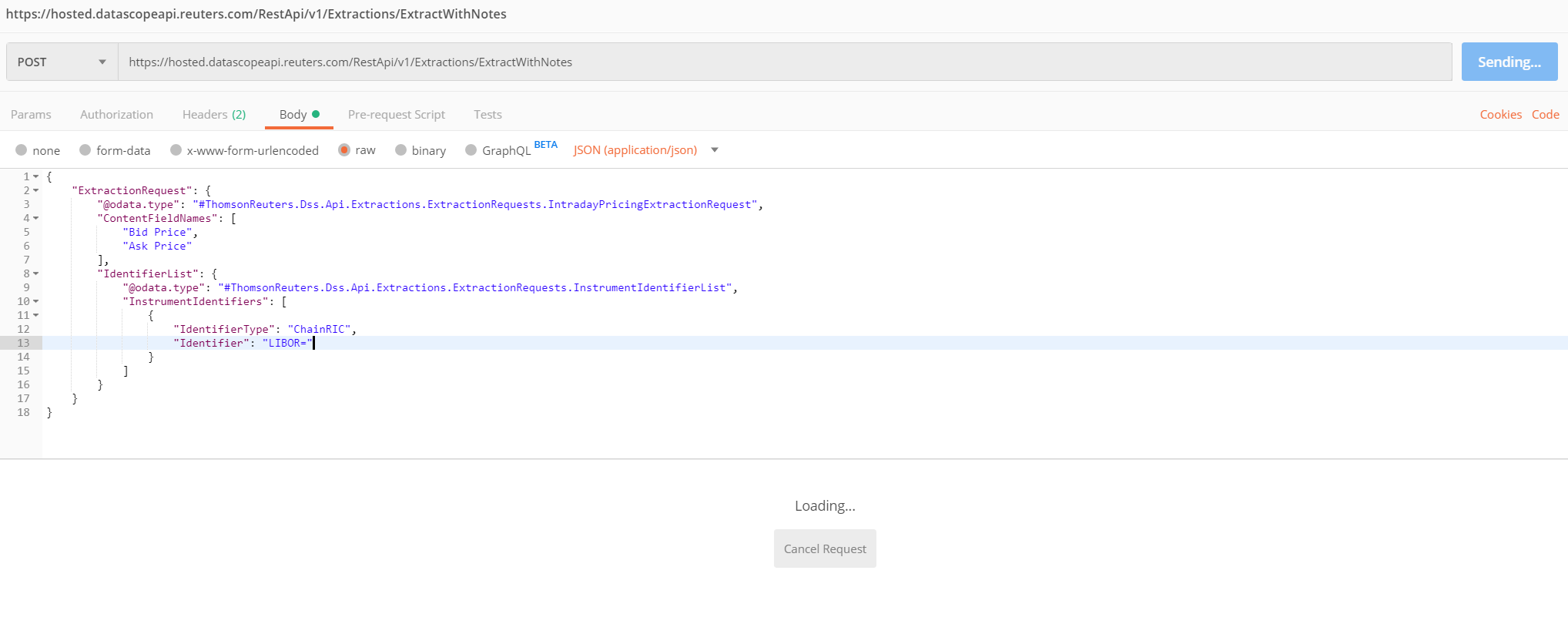

Hi @beatgtech,

You can use chain RIC: LIBOR= to extract all LIBOR rates. Below is the sample of request.

{

"ExtractionRequest": {

"@odata.type": "#ThomsonReuters.Dss.Api.Extractions.ExtractionRequests.IntradayPricingExtractionRequest",

"ContentFieldNames": [

"Bid Price",

"Ask Price"

],

"IdentifierList": {

"@odata.type": "#ThomsonReuters.Dss.Api.Extractions.ExtractionRequests.InstrumentIdentifierList",

"InstrumentIdentifiers": [

{

"IdentifierType": "ChainRIC",

"Identifier": "LIBOR="

}

]

}

}

}

{kind=link}

{kind=link}

{kind=link}