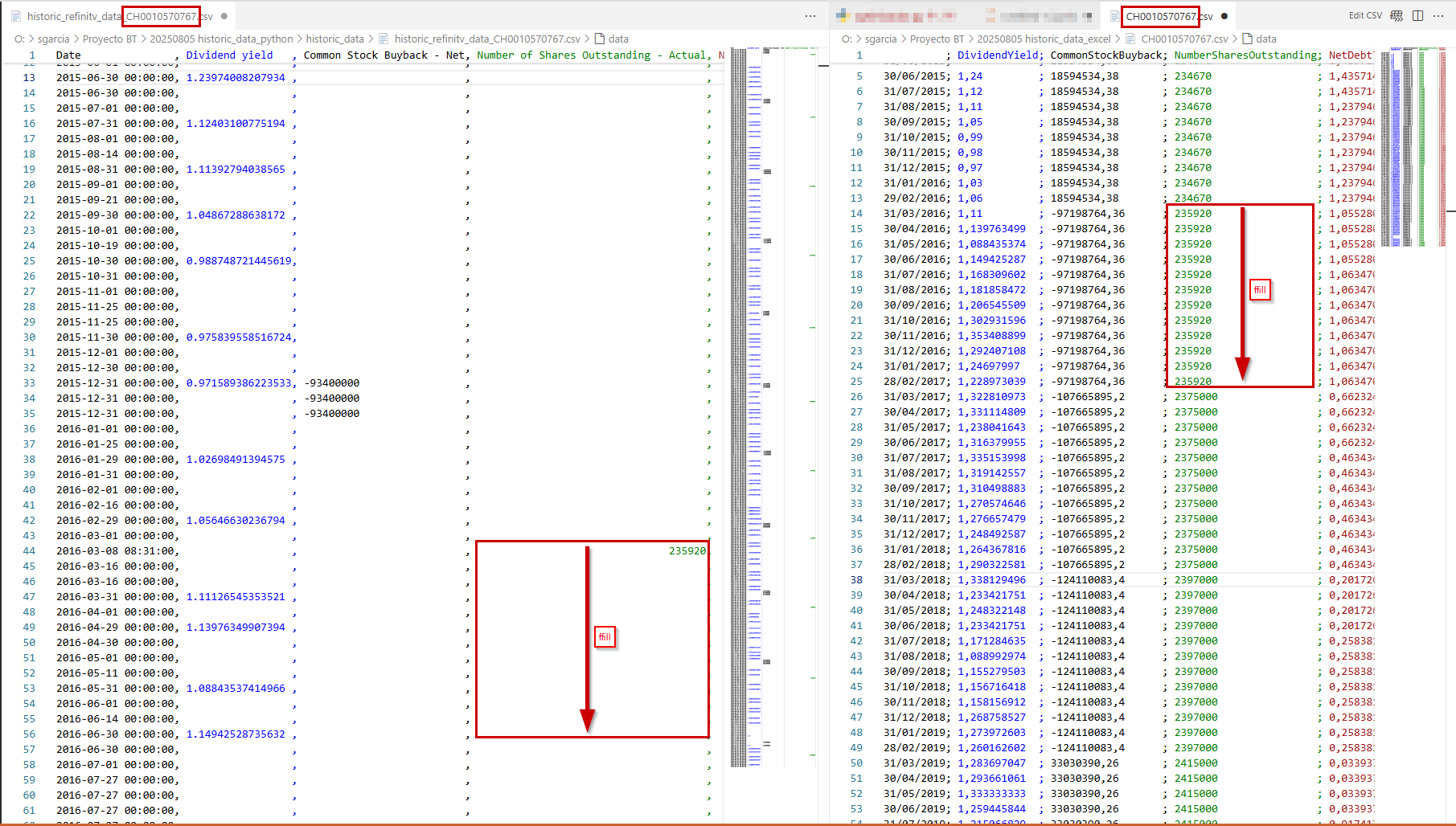

What I want is to download the data for 3K ISINs. That can be done using Python.if I use python I don't get auto-imputed data.

Below is the Python code client is refering

import refinitiv.data as rdfrom tqdm import tqdmfor isin in tqdm(isins):try:response = rd.get_history(universe=[isin.strip()],fields=["TR.DividendYield","TR.F.ComStockBuybackNet","TR.NumberofSharesOutstandingActual","TR.NetDebtToEBITDA","TR.FreeCashFlow","TR.SharesOutstanding","TR.F.PriceToCFPerShr","TR.PCReturnOnInvestedCapPct","TR.WACC","TR.CompanyMarketCap","AVAIL(TR.F.IntrCovRatioTTM(AlignType=PeriodEndDate),TR.F.IntrCovRatio(AlignType=PeriodEndDate, Period=FY0))","AVAIL(TR.DPSMean( AlignType=PeriodEndDate, Methodology=InterimSum, Period=NTM),TR.DPSMean(AlignType=PeriodEndDate, Methodology=WeightedAnnual, Period=NTM))","TR.F.DPSComGrossIssue5YrCAGR(AlignType=PeriodEndDate, InstrumentType=Primary)","AVAIL(TR.F.EVToLeveredFOCFTTM(AlignType=PeriodEndDate),TR.F.EVToLeveredFOCF(AlignType=PeriodEndDate, Period=FY0))","AVAIL(TR.F.FOCFYldPctTTM(AlignType=PeriodEndDate),TR.F.FOCFYldPct(AlignType=PeriodEndDate, Period=FY0))","TR.FreeFloatPct","TR.Volume",],start="2015-05-29",end="2025-06-03",interval = "monthly")response.to_csv(f"historic_data/historic_refinitv_data_{isin}.csv")except Exception as ex:print(ex)with open("historic_data/errores.csv", "a") as file:file.write(f"{isin}\n")