My client is currently trying out the codebook + API (which are extremely nice by the way) and she is running through a weird observation:

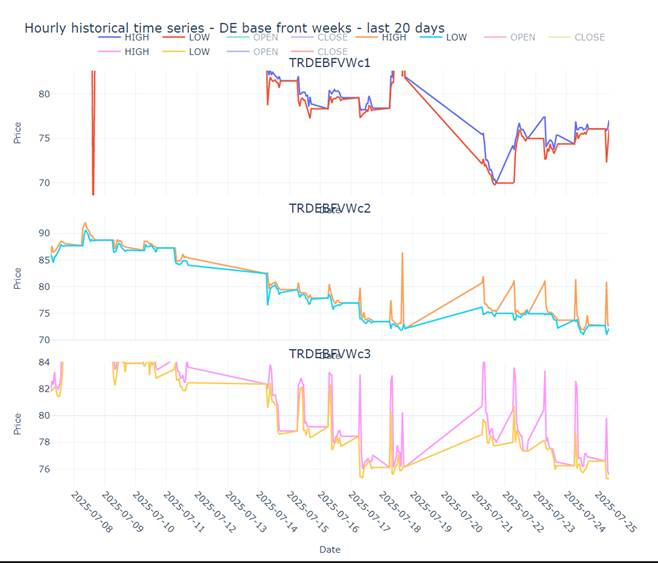

The week+2 and week+3 show very weird “HIGH” prices that I do not find were traded on the market at the timestamp thy should be.

For rolling c2 and c3 RIC codes, is there something specific to be taken into account ? (for ex, could be mixed with the front month?)

Do you know if PC data will be added later?

Thank you and kind regards,