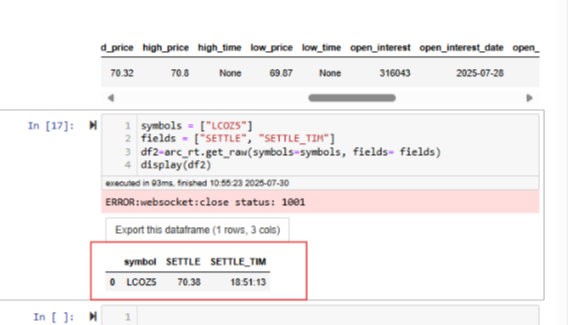

We've been having some issues with live data from RDMS. Basically, we look at refinitiv as close to 7:30 PM UK time as possible to estimate the settlement price for brent.

For example for Dec brent (LCOZ5) - we were expecting the settlement price of 70.38 and the value we got back was 70.18.

The price we got appeared to be a delayed price.