QPS Financial Contracts API - Structured Products error message: Invalid Correlation Data.

Hello team,

I keep getting the following error message while pricing structured products using QPS financial contracts API:

'Cannot price Structured Products. Invalid correlation data.'

It seems that when there are more than one Equity underliers the error would be triggered. I have priced similar products with single equity underlier with no issues.

Request body below.

{

"fields": [

"MarketValueInDealCcy",

"ErrorMessage"

],

"universe": [

{

"instrumentDefinition": {

"instrumentTag": "63873HEZ3",

"dealCcy": "USD",

"inputs": [

{

"type": "string",

"name": "CUSIP",

"value": "63873HEZ3"

},

{

"type": "string",

"name": "Issuer",

"value": "MS"

},

{

"type": "string",

"name": "Callable",

"value": "True"

},

{

"type": "string",

"name": "PrincipalAtRisk",

"value": "True"

},

{

"type": "string",

"name": "RangeAccrualType",

"value": "A"

},

{

"type": "string",

"name": "SOFR",

"value": "False"

},

{

"type": "string",

"name": "NumOfAssets",

"value": "2"

},

{

"type": "date",

"name": "TradeDate",

"value": "28/03/2016"

},

{

"type": "date",

"name": "ValuationDate",

"value": "26/03/2036"

},

{

"type": "date",

"name": "MaturityDate",

"value": "31/03/2036"

},

{

"type": "date",

"name": "StartDate",

"value": "31/03/2016"

},

{

"type": "date",

"name": "EndDate",

"value": "31/03/2036"

},

{

"type": "date",

"name": "RangeStart",

"value": "31/03/2020"

},

{

"type": "date",

"name": "RangeStart_2",

"value": "31/03/2026"

},

{

"type": "date",

"name": "CallStart",

"value": "31/03/2017"

},

{

"type": "date",

"name": "CallEnd",

"value": "31/03/2036"

},

{

"type": "string",

"name": "CMS_Long",

"value": "30Y"

},

{

"type": "string",

"name": "CMS_Short",

"value": "2Y"

},

{

"type": "string",

"name": "CpnB",

"value": "0.65"

},

{

"type": "string",

"name": "Trigger",

"value": "0.5"

},

{

"type": "string",

"name": "FixedCpn",

"value": "0.09"

},

{

"type": "string",

"name": "Cap",

"value": "0.1"

},

{

"type": "string",

"name": "Notional",

"value": "100"

},

{

"type": "string",

"name": "PayFreq",

"value": "M"

},

{

"type": "string",

"name": "CallFreq",

"value": "Q"

},

{

"type": "string",

"name": "CallGap",

"value": "-5B"

},

{

"type": "string",

"name": "ResetGap",

"value": "-2B"

},

{

"type": "string",

"name": "PayGap",

"value": "0B"

},

{

"type": "string",

"name": "DateRule",

"value": "ModifiedFollowing"

},

{

"type": "string",

"name": "Calendar",

"value": "NYSE"

},

{

"type": "string",

"name": "DayCount",

"value": "Act/Act"

},

{

"type": "string",

"name": "A_1",

"value": "SP500"

},

{

"type": "string",

"name": "A_2",

"value": "RUT"

},

{

"type": "string",

"name": "Initial_1",

"value": "2037.05"

},

{

"type": "string",

"name": "Initial_2",

"value": "1093.6"

},

{

"type": "string",

"name": "ResetArrear",

"value": "False"

},

{

"type": "string",

"name": "Leverage_Steps",

"value": "2"

},

{

"type": "string",

"name": "Leverage",

"value": "8.0"

},

{

"type": "string",

"name": "Leverage_2",

"value": "10.0"

},

{

"type": "string",

"name": "Spread",

"value": "0.0"

}

],

"payoffDescription": [

[

"Schedule type",

"Schedule description",

"Spot_1",

"Spot_2",

"WorstPerform",

"CMS_Spread",

"nday",

"Actday",

"Cpn",

"Redemption",

"Price"

],

[

"AtDate",

"TradeDate",

"Initial_1",

"Initial_2",

"",

"",

"$n=0",

"$act=0",

"",

"",

""

],

[

"AllTheTime",

"FromTo(RangeStart,MaturityDate,1b)",

"EqSpot(A_1)",

"EqSpot(A_2)",

"MIN(Spot_1[t]/Spot_1[1],Spot_2[t]/Spot_2[1])",

"",

"$n=$n+IF(WorstPerform[t]>=CpnB,1,0)",

"$act=$act+1",

"",

"",

""

],

[

"OnSchedule",

"DateTable(StartDate,RangeStart,PayFreq,DayCount,PayGap:=PayGap,ResetGap:=ResetGap,Arrear:=Yes,DateRule:=DateRule,Calendar:=Calendar)",

"",

"",

"",

"",

"",

"",

"FixedCpn*InterestTerm()",

"",

"Receive Notional*Cpn[t]"

],

[

"OnSchedule",

"DateTable(StartDate,EndDate,PayFreq,DayCount,PayGap:=PayGap,ResetGap:=ResetGap,Arrear:=Yes,DateRule:=DateRule,Calendar:=Calendar)",

"",

"",

"",

"Max(0,SwapRate(USD,EventDate(),CMS_Long)-SwapRate(USD,EventDate(),CMS_Short)+Spread)",

"",

"",

"",

"",

""

],

[

"OnSchedule",

"DateTable(RangeStart,RangeStart_2,PayFreq,DayCount,PayGap:=PayGap,ResetGap:=0B,Arrear:=Yes,DateRule:=DateRule,Calendar:=Calendar)",

"",

"",

"",

"",

"",

"",

"$n/$act*Min(Cap,Leverage*IF(\"ResetArrear\"==\"False\",CMS_Spread[LastDate(-1)],CMS_Spread[LastDate]))*InterestTerm()",

"",

"Receive Notional*Cpn[t];$n=0;$act=0"

],

[

"OnSchedule",

"DateTable(RangeStart_2,EndDate,PayFreq,DayCount,PayGap:=PayGap,ResetGap:=0B,Arrear:=Yes,DateRule:=DateRule,Calendar:=Calendar)",

"",

"",

"",

"",

"",

"",

"$n/$act*Min(Cap,Leverage_2*IF(\"ResetArrear\"==\"False\",CMS_Spread[LastDate(-1)],CMS_Spread[LastDate]))*InterestTerm()",

"",

"Receive Notional*Cpn[t];$n=0;$act=0"

],

[

"OnSchedule",

"DateTable(CallStart,CallEnd,CallFreq,DayCount,PayGap:=PayGap,ResetGap:=CallGap,Arrear:=False,DateRule:=DateRule,Calendar:=Calendar)",

"",

"",

"",

"",

"",

"",

"",

"",

"CallableBy(Them,Notional)"

],

[

"AtDate",

"ValuationDate",

"EqSpot(A_1)",

"EqSpot(A_2)",

"MIN(Spot_1[t]/Spot_1[1],Spot_2[t]/Spot_2[1])",

"",

"",

"",

"",

"IF(WorstPerform[t]>=Trigger,1,WorstPerform[t])",

"Receive(MaturityDate,Notional*Redemption[t])"

]

]

},

"pricingParameters": {

"models": [

{

"underlyingCode": "USD",

"underlyingName": "USD",

"underlyingCurrency": "USD",

"assetClass": "InterestRate",

"modelName": "HullWhite1Factor",

"modelParameters": {

"volatilityTermStructure": [

{

"value": 1.0,

"unit": "Percent"

}

],

"meanReversionTermStructure": [

{

"value": 1.0,

"unit": "Percent"

}

],

"volatilityModel": "NormalVolatility"

}

},

{

"underlyingCode": ".RUT",

"underlyingName": "RUT",

"underlyingCurrency": "USD",

"assetClass": "Equity",

"modelName": "Dupire"

},

{

"underlyingCode": ".SPX",

"underlyingName": "SP500",

"underlyingCurrency": "USD",

"assetClass": "Equity",

"modelName": "Dupire"

}

],

"numericalMethod": {

"allTheTimePointsPerYear": 260,

"method": "AmericanMonteCarlo",

"additionalPoints": 12,

"simulationCount": 1000

},

"fundingSpreadInBp": 0,

"forceDecreasingDiscountFactor": false,

"includeCashFlowsAtValuationDate": false,

"correlationReferenceCoefficientPercent": -100,

"correlationMultiplier": 1,

"numeraireType": "Cash",

"useBasisSwap": false,

"valuationDate": "2022-09-01"

},

"instrumentType": "StructuredProduct"

}

]

}

Answers

-

Hi @Harry.Nan

I had simillar issues in the past, and wrote this article as a result:

Troubleshooting IPA & RD Python Library: https://developers.lseg.com/en/article-catalog/article/troubleshooting-ipa-and-the-data-library-api-in-python

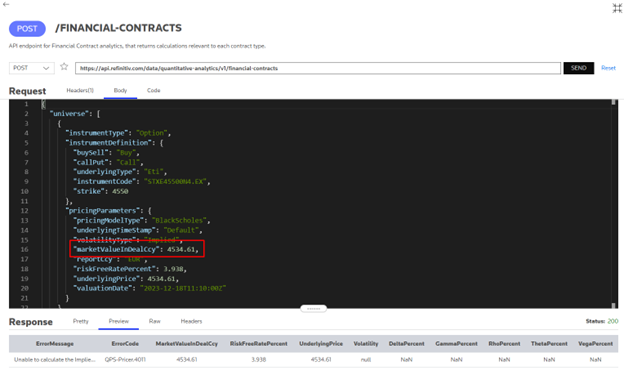

The way I found the culprit in my body was through trial and error. I would suggest the same here. I wrote about just this at the end of the article:I recently came uppon a second error returned from IPA, ''ErrorMessage" `Unable to calculate the Implied Volatility` and "ErrorCode" `QPS-Pricer.4011`.I went through the technique above, and found the folowing test call totry out on the API Playground:{"universe": [{"instrumentType": "Option","instrumentDefinition": {"buySell": "Buy","callPut": "Call","underlyingType": "Eti","instrumentCode": "STXE45500N4.EX","strike": 4550},"pricingParameters": {"pricingModelType": "BlackScholes","underlyingTimeStamp": "Default","volatilityType": "Implied","marketValueInDealCcy": 4534.61,"reportCcy": "EUR","riskFreeRatePercent": 3.938,"underlyingPrice": 4534.61,"valuationDate": "2023-12-18T11:10:00Z"}}],"fields": ["ErrorMessage","ErrorCode","MarketValueInDealCcy","RiskFreeRatePercent","UnderlyingPrice","Volatility","DeltaPercent","GammaPercent","RhoPercent","ThetaPercent","VegaPercent"]}What I then did, on the Playground, was remove one (and only one) argument. I found out, through this trial and error proccess that the the culprit was "marketValueInDealCcy".

Removing this argument showed that this option was trading at a much lower rate, making Greeks imposible to calculate.Please do let me know if you did not find the culprit argument in the body after going through the above.

0 -

Hi Jonathan, thank you for your reply. I've tried everything I could. Is there a way to get a more detailed error message/log so I can figure out what failed during the pricing process?

The following request with almost the same structure works, only difference being that it only has one equity index underliers rather than two in the original one I posted. I am struggling to understand what triggers the specific 'Invalid Correlation Data' error.

{

"fields": [

"MarketValueInDealCcy",

"ErrorMessage"

],

"universe": [

{

"instrumentDefinition": {

"instrumentTag": "1730T02P3",

"dealCcy": "USD",

"inputs": [

{

"type": "string",

"name": "CUSIP",

"value": "1730T02P3"

},

{

"type": "string",

"name": "Issuer",

"value": "C"

},

{

"type": "string",

"name": "Callable",

"value": "True"

},

{

"type": "string",

"name": "PrincipalAtRisk",

"value": "False"

},

{

"type": "string",

"name": "RangeAccrualType",

"value": "A"

},

{

"type": "string",

"name": "SOFR",

"value": "False"

},

{

"type": "string",

"name": "NumOfAssets",

"value": "1"

},

{

"type": "date",

"name": "TradeDate",

"value": "28/10/2014"

},

{

"type": "date",

"name": "ValuationDate",

"value": "31/10/2034"

},

{

"type": "date",

"name": "MaturityDate",

"value": "31/10/2034"

},

{

"type": "date",

"name": "StartDate",

"value": "31/10/2014"

},

{

"type": "date",

"name": "EndDate",

"value": "31/10/2034"

},

{

"type": "date",

"name": "RangeStart",

"value": "31/10/2015"

},

{

"type": "date",

"name": "CallStart",

"value": "31/10/2015"

},

{

"type": "date",

"name": "CallEnd",

"value": "31/10/2034"

},

{

"type": "string",

"name": "CMS_Long",

"value": "30Y"

},

{

"type": "string",

"name": "CMS_Short",

"value": "2Y"

},

{

"type": "string",

"name": "CpnB",

"value": "0.7"

},

{

"type": "string",

"name": "FixedCpn",

"value": "0.09"

},

{

"type": "string",

"name": "Cap",

"value": "0.1"

},

{

"type": "string",

"name": "Notional",

"value": "100"

},

{

"type": "string",

"name": "PayFreq",

"value": "Q"

},

{

"type": "string",

"name": "CallFreq",

"value": "Q"

},

{

"type": "string",

"name": "CallGap",

"value": "-5B"

},

{

"type": "string",

"name": "ResetGap",

"value": "-2B"

},

{

"type": "string",

"name": "PayGap",

"value": "0B"

},

{

"type": "string",

"name": "DateRule",

"value": "ModifiedFollowing"

},

{

"type": "string",

"name": "Calendar",

"value": "NYSE"

},

{

"type": "string",

"name": "DayCount",

"value": "30/360"

},

{

"type": "string",

"name": "A_1",

"value": "SP500"

},

{

"type": "string",

"name": "Initial_1",

"value": "1985.05"

},

{

"type": "string",

"name": "ResetArrear",

"value": "False"

},

{

"type": "string",

"name": "Leverage_Steps",

"value": "1"

},

{

"type": "string",

"name": "Leverage",

"value": "4.0"

},

{

"type": "string",

"name": "Spread",

"value": "0.0"

}

],

"payoffDescription": [

[

"Schedule type",

"Schedule description",

"Spot_1",

"WorstPerform",

"CMS_Spread",

"nday",

"Actday",

"Cpn",

"Redemption",

"Price"

],

[

"AtDate",

"TradeDate",

"Initial_1",

"",

"",

"$n=0",

"$act=0",

"",

"",

""

],

[

"AllTheTime",

"FromTo(RangeStart,MaturityDate,1b)",

"EqSpot(A_1)",

"Spot_1[t]/Spot_1[1]",

"",

"$n=$n+IF(WorstPerform[t]>=CpnB,1,0)",

"$act=$act+1",

"",

"",

""

],

[

"OnSchedule",

"DateTable(StartDate,RangeStart,PayFreq,DayCount,PayGap:=PayGap,ResetGap:=ResetGap,Arrear:=Yes,DateRule:=DateRule,Calendar:=Calendar)",

"",

"",

"",

"",

"",

"FixedCpn*InterestTerm()",

"",

"Receive Notional*Cpn[t]"

],

[

"OnSchedule",

"DateTable(StartDate,EndDate,PayFreq,DayCount,PayGap:=PayGap,ResetGap:=ResetGap,Arrear:=Yes,DateRule:=DateRule,Calendar:=Calendar)",

"",

"",

"Max(0,SwapRate(USD,EventDate(),CMS_Long)-SwapRate(USD,EventDate(),CMS_Short)+Spread)",

"",

"",

"",

"",

""

],

[

"OnSchedule",

"DateTable(RangeStart,EndDate,PayFreq,DayCount,PayGap:=PayGap,ResetGap:=0B,Arrear:=Yes,DateRule:=DateRule,Calendar:=Calendar)",

"",

"",

"",

"",

"",

"$n/$act*Min(Cap,Leverage*IF(\"ResetArrear\"==\"False\",CMS_Spread[LastDate(-1)],CMS_Spread[LastDate]))*InterestTerm()",

"",

"Receive Notional*Cpn[t];$n=0;$act=0"

],

[

"OnSchedule",

"DateTable(CallStart,CallEnd,CallFreq,DayCount,PayGap:=PayGap,ResetGap:=CallGap,Arrear:=False,DateRule:=DateRule,Calendar:=Calendar)",

"",

"",

"",

"",

"",

"",

"",

"CallableBy(Them,Notional)"

],

[

"AtDate",

"ValuationDate",

"EqSpot(A_1)",

"Spot_1[t]/Spot_1[1]",

"",

"",

"",

"",

"1",

"Receive(MaturityDate,Notional*Redemption[t])"

]

]

},

"pricingParameters": {

"models": [

{

"underlyingCode": "USD",

"underlyingName": "USD",

"underlyingCurrency": "USD",

"assetClass": "InterestRate",

"modelName": "HullWhite1Factor",

"modelParameters": {

"volatilityTermStructure": [

{

"value": 1.0,

"unit": "Percent"

}

],

"meanReversionTermStructure": [

{

"value": 1.0,

"unit": "Percent"

}

],

"volatilityModel": "NormalVolatility"

}

},

{

"underlyingCode": ".SPX",

"underlyingName": "SP500",

"underlyingCurrency": "USD",

"assetClass": "Equity",

"modelName": "Dupire"

}

],

"numericalMethod": {

"allTheTimePointsPerYear": 260,

"method": "AmericanMonteCarlo",

"additionalPoints": 12,

"simulationCount": 1000

},

"fundingSpreadInBp": 0,

"forceDecreasingDiscountFactor": false,

"includeCashFlowsAtValuationDate": false,

"correlationReferenceCoefficientPercent": -100,

"correlationMultiplier": 0.995,

"numeraireType": "Cash",

"useBasisSwap": false,

"valuationDate": "2022-09-01"

},

"instrumentType": "StructuredProduct"

}

]

}0 -

Hi @Harry.Nan

Thank you for your reply. I have let the internal IPA team know of this and kept you in the email exchange on this matter. They are investigating the issue and will get back as soon as there is news.

0

Categories

- All Categories

- 3 Polls

- 6 AHS

- 37 Alpha

- 167 App Studio

- 6 Block Chain

- 4 Bot Platform

- 18 Connected Risk APIs

- 47 Data Fusion

- 34 Data Model Discovery

- 707 Datastream

- 1.5K DSS

- 633 Eikon COM

- 5.2K Eikon Data APIs

- 15 Electronic Trading

- 1 Generic FIX

- 7 Local Bank Node API

- 7 Trading API

- 3K Elektron

- 1.5K EMA

- 260 ETA

- 571 WebSocket API

- 41 FX Venues

- 16 FX Market Data

- 2 FX Post Trade

- 1 FX Trading - Matching

- 12 FX Trading – RFQ Maker

- 5 Intelligent Tagging

- 2 Legal One

- 26 Messenger Bot

- 4 Messenger Side by Side

- 9 ONESOURCE

- 7 Indirect Tax

- 60 Open Calais

- 284 Open PermID

- 47 Entity Search

- 2 Org ID

- 1 PAM

- PAM - Logging

- 6 Product Insight

- Project Tracking

- ProView

- ProView Internal

- 25 RDMS

- 2.2K Refinitiv Data Platform

- 17 CFS Bulk File/TM3

- 904 Refinitiv Data Platform Libraries

- 5 LSEG Due Diligence

- 1 LSEG Due Diligence Portal API

- 4 Refinitiv Due Dilligence Centre

- Rose's Space

- 1.2K Screening

- 18 Qual-ID API

- 13 Screening Deployed

- 23 Screening Online

- 12 World-Check Customer Risk Screener

- 1K World-Check One

- 46 World-Check One Zero Footprint

- 45 Side by Side Integration API

- 2 Test Space

- 3 Thomson One Smart

- 10 TR Knowledge Graph

- 151 Transactions

- 143 REDI API

- 1.8K TREP APIs

- 4 CAT

- 27 DACS Station

- 126 Open DACS

- 1.1K RFA

- 108 UPA

- 197 TREP Infrastructure

- 232 TRKD

- 921 TRTH

- 5 Velocity Analytics

- 9 Wealth Management Web Services

- 106 Workspace SDK

- 11 Element Framework

- 5 Grid

- 19 World-Check Data File

- 1 Yield Book Analytics

- 48 中文论坛