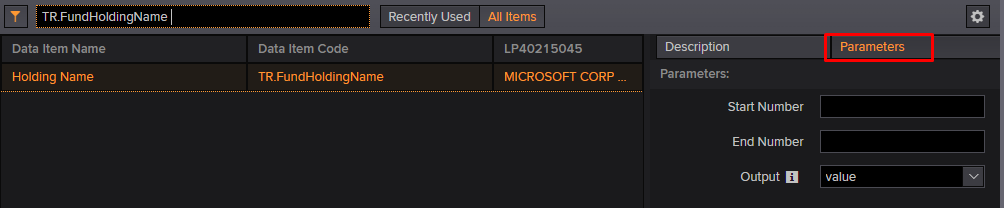

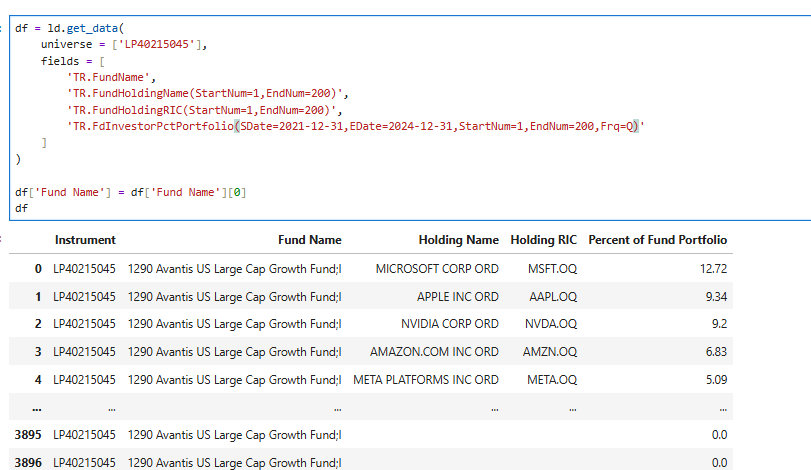

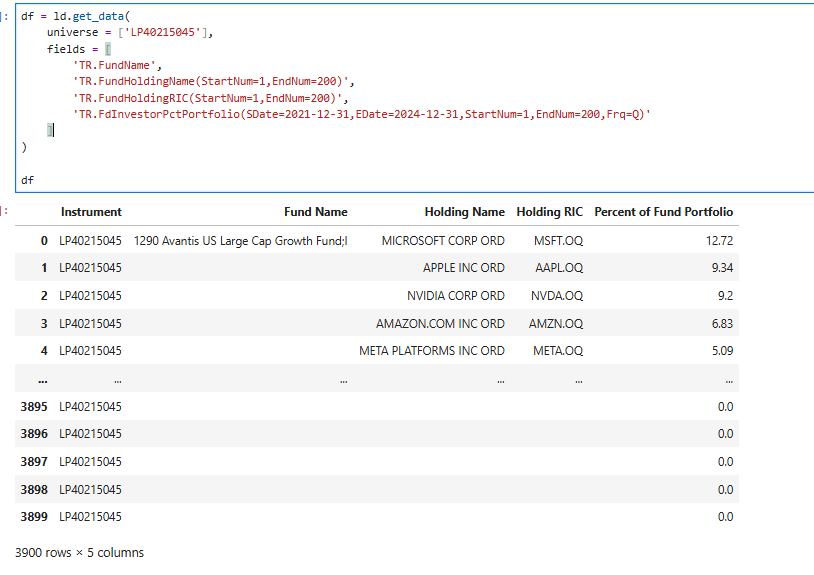

Hi everyone, I am a researcher at the Catholic University of Milan, currently working on a project that involves historical holdings data for U.S. actively managed mutual funds. Specifically, I require the full holdings information (not just the top 3 holdings) for all such mutual funds, on a quarterly basis over the past 20 years, if available. I would like to ask whether it is possible to retrieve this data using an API. Given the volume of data involved, I understand that it may not be feasible to extract everything in a single call. I would therefore like to ask if it is possible to build a Python routine to download the data in blocks (e.g., retrieving the full time series for 10 mutual funds at a time) and then append the results automatically—without having to perform the process manually. I have attached a screenshot of the code I have been using so far. Thank you in advance for your support. Best regards, Mema Myftar